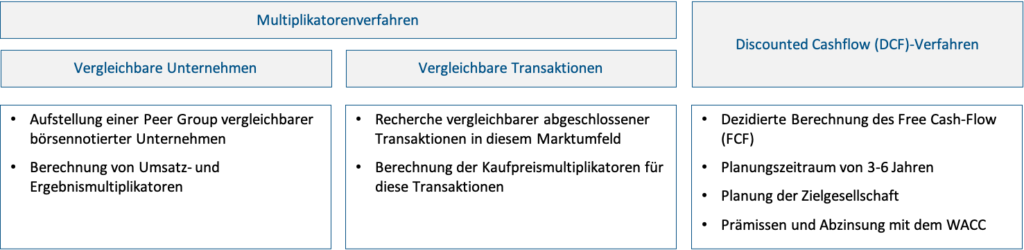

Multiplier methods

Multiplier methods are simple and quick ways of valuing a business, which is why they are frequently used in practice. The multipliers, often referred to as multiples, are derived more or less systematically from a group of comparable companies. These may be comparable listed companies or transactions involving shares in comparable (unlisted) companies.

In practice, three multipliers are used:

- Revenue multiple – When companies are growing rapidly and/or no positive earnings figures are available

- EBITDA multiple – For companies with cyclical investment behaviour

- EBIT multiple – For companies where investments occur regularly or play a minor role

In most cases, EBIT is used as the basis for valuing established companies, as EBIT comes closest to cash flow when capital expenditure is roughly equal to depreciation.

Of course, it must always be borne in mind that the EBIT for a given year often does not represent the ‘true’ company result. For this reason, EBIT is normalised, meaning that extraordinary income and expenditure or special influences from shareholders (for example, salaries, vehicles, rent) are excluded from the profit and loss account.

Furthermore, the reference year has a significant impact on the value. As a rule, the current financial year is used (current forecast). If only one year is used, growth potential or cyclical trends may not be adequately taken into account. Therefore, adjustments may be necessary to arrive at an appropriate basis.

If the potential is sufficiently concrete, it can be adjusted. In some cases, averages over several years may be used, taking into account both planning and past performance. This allows companies to be valued appropriately during periods of economic volatility.

Comparable Transaction Analysis

The first method is based on comparable transactions (also known as Comparable Transactions). To form the peer group, transactions involving companies from the same industry are considered. This method is based on the idea that multiples paid in the past for transactions that have already been completed also reflect the ‘appropriate market price today’.

The approach of valuing companies based on comparable transactions has significant strengths when it comes to valuing unlisted companies, which are usually much smaller, more focused and have a more regional focus than their generally much larger, more broadly diversified and more international listed competitors.

Unfortunately, however, the valuation method also presents difficulties in practice:

- The available information is often insufficient, as details of transactions involving private companies are frequently not published, or not published in full.

- The time period from which the transactions are drawn must be very long in order to obtain a representative data set. As the valuation of sectors changes over time (e.g. because interest rates, technologies and growth prospects change), values determined in this way may differ from the current value.

Comparable listed companies

The second method is based on the valuation of comparable listed companies (also known as trading multiples or trading comparables). The rationale behind this method is similar to that of valuation using transactions involving comparable companies:

The consultant creates a peer group of listed companies that correspond as closely as possible to the company being valued. In this method, the multiple is calculated as a multiple of the market capitalisation of the financial metric (EBITDA or EBIT) of the listed peer companies.

This method offers the advantage that the data for listed companies is up to date, fully publicly available and relatively easy to collect.

The drawback lies in the fact that listed companies are often very difficult to compare with a German unlisted SME. Imagine comparing Coca-Cola with a medium-sized, regional drinks manufacturer in Germany. Are the differences not greater than the similarities? Compared to listed companies, SMEs are often more regional, smaller and more focused. Furthermore, shares in listed companies are highly fungible, i.e. they can be sold at any time in variable quantities without delay and at minimal transaction costs.

Discounted Cash Flow (DCF) method

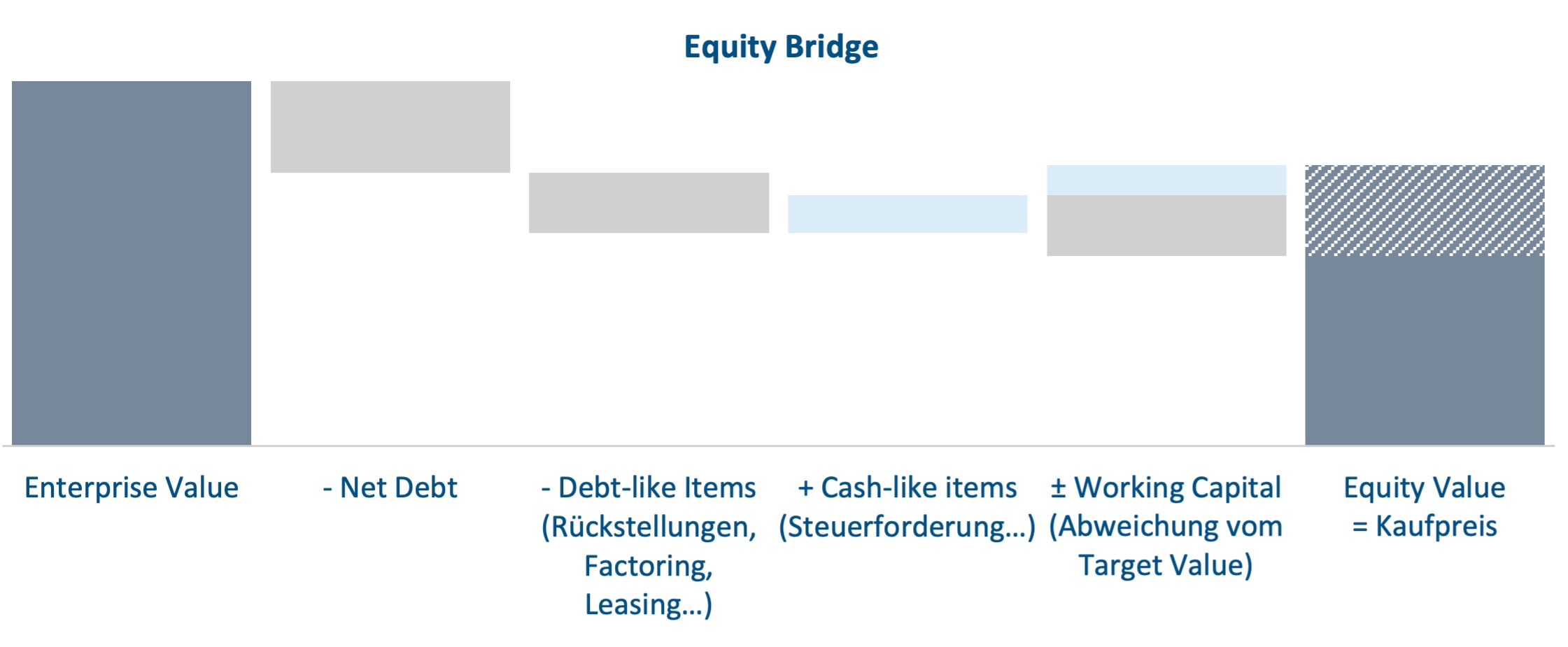

To calculate the enterprise value using the Discounted Cash Flow (DCF) method, the company’s future cash flows are forecast and discounted using a risk-adjusted cost of capital. In the DCF method, the enterprise value is essentially determined by the cash flow assumed to be sustainable at the end of the detailed forecast period (‘perpetual annuity’). The present value of this perpetual annuity can account for 60–70% of the enterprise value. In contrast to the discounted cash flow method, the income approach is based not on cash surpluses but on earnings or net profits. In a typical M&A process, the income approach plays hardly any role. In the discounted cash flow (DCF) method, gross approaches dominate in the M&A environment, whereby cash flows to equity and debt providers (so-called free cash flows) are discounted using the weighted cost of capital (weighted average cost of capital or WACC). The purchase price payable to equity investors is then determined by deducting net financial debt from the enterprise value calculated in this way.

The strength of this method lies in its accuracy, as it provides a comprehensive projection of a company’s future development, including future investments and changes in working capital. For this reason, it is also the method favoured in valuation theory.

In practice, however, this method often encounters difficulties. Firstly, the cost of capital is derived from comparable listed companies. These are only transferable to medium-sized companies to a very limited extent for the reasons already mentioned above, such as size, diversification, fungibility, etc. Secondly, the planning period of 3-5 years involves planning effort and corresponding uncertainty.

Net Asset Value Method and Non-Operating Assets

The company valuation methods mentioned so far assume that all assets transferred with the company are necessary to achieve the planned EBIT results. This naturally also includes inventories within the usual range of coverage. The value of these assets is therefore included in the company value and does not need to be considered separately. Therefore, the net asset value method is generally not used in company valuations.

However, the situation is different when there are non-core assets: The value of these assets can be realized in addition to the company value.

When selling a company with significant real estate assets, the net asset value of these properties may also be relevant in some circumstances. If the net asset value of the real estate assets is high, it may be advisable in the event of a transaction to separate them out beforehand and then sell them separately or rent them to the new company owner.

Liquidation Value Method in Company Valuation

The liquidation value is calculated from the value of the individual assets less the liquidation costs.

The liquidation value method is only used to determine the company value if the values of the multiples or DCF methods are below the liquidation value. In concrete terms, this means that it appears more profitable to sell the company’s assets than to continue the business.